South China Annual Report: PTA is slow and difficult to have a trend

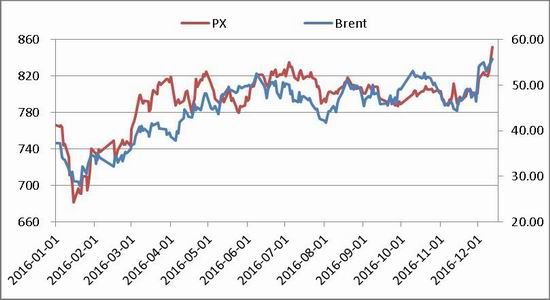

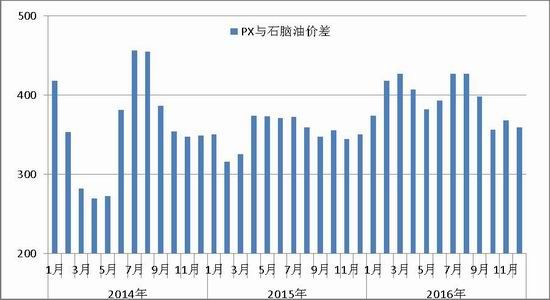

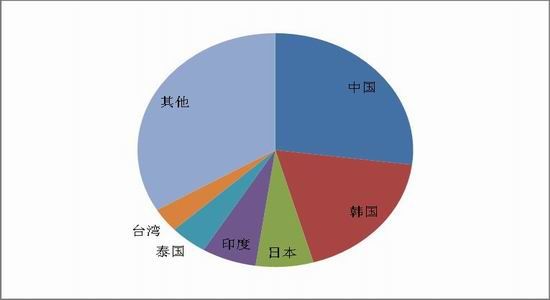

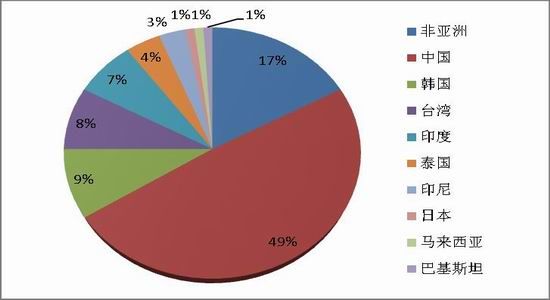

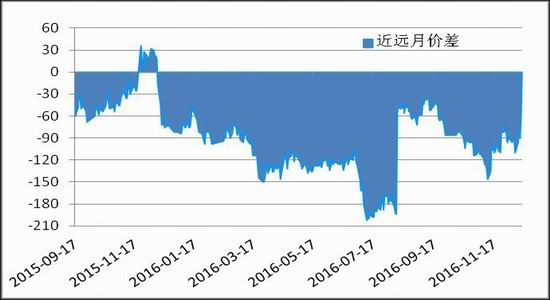

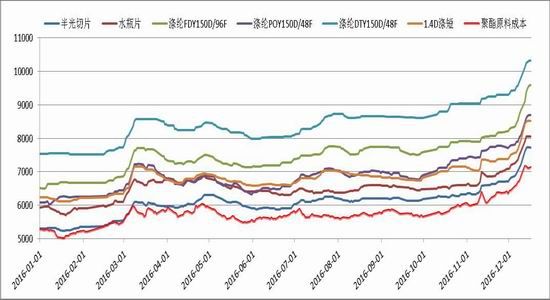

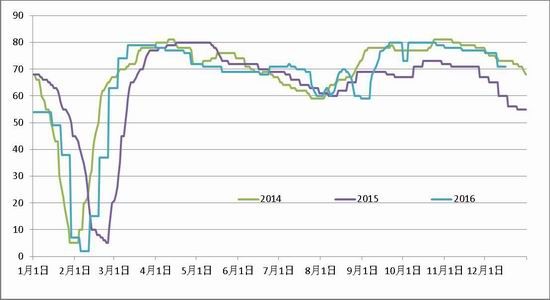

Client Summary In 2016, the domestic economy was running smoothly. It is expected that the annual GDP growth rate will be around 6.7%. The supply-side structural reform will be solidly promoted, and commodity prices will rebound. After two years of shocks at the bottom, PTA prices finally began to rise in the fourth quarter of 2006 with the rebound in crude oil prices and strong demand for polyester, but the volatility also increased. In terms of the industrial chain, crude oil stopped falling and rebounded. Although PX improved its efficiency, it remained relatively weak. The supply and demand pattern of PTA was slightly destocked throughout the year. The benefits of polyester products were improved compared with 2015, and the inventory continued to decrease. In 2017, PTA's new capacity was not much. Some of the long-term parking devices were expected to resume production. The downstream consumption growth rate continued to slow down. There is no big contradiction in the overall PTA supply and demand pattern. Next year, we will focus on the changes in crude oil prices. If the focus continues to move up, then the PTA will also move up the center, which will easily rise and fall. Chapter 1 2016 PTA Futures Market Review 1.1. Overview Figure 1.1.1: 2016 PTA futures main contract trend Source: Wenhua Finance & Nanhua Research Since the second half of 2014, as the price of crude oil has plummeted, the cost of PTA has collapsed. The price of PTA has also experienced a sharp decline. In 2015, PTA prices began to oscillate and bottomed out. This year, the PTA price center has slowly risen. Looking back at the trend of PTA futures in 2016, it can be divided into four stages. The first phase is the price recovery phase from January to April, the second phase is the rapid correction down phase in May, the third phase is the interval turbulence phase from June to October, and the fourth phase is the gravity center upshift phase from November to December. . Overall, compared to the price of less than 5,000 yuan / ton at the beginning of the year, the price of the whole year has risen slightly. 1.2. The first phase (price rises in January-April) In January, the PTA price was still at a low level. The TA1605 main contract hit a record low of 4,200 yuan/ton in the month, and the spot price also fell to around 4,100 yuan/ton. Then, driven by the rebound of crude oil, the price of the cost side moved up, and the price of PTA stabilized slightly. Although the traditional Spring Festival is off season in February, the price of PTA continues to rise due to the strong rebound in crude oil prices, and PTA prices continue to rise. The PTA price continued to rebound in March, coupled with the promotion of funds, the increase in demand for polyester and the shutdown of some devices, the PTA price was consolidating at a high level. In April, with the resumption of the new installation of Hanbang and other factors, and the strong financial strength, the PTA price continued to rise, and the price once hit a new high for the year. 1.3. Second stage (prices fell rapidly in May) In May, PTA prices followed the downward trend of bulk commodities as a whole, changing the pattern of crazy growth and turning heads down into a rapid decline adjustment pattern. In addition, the new equipment of Hanbang PTA was successfully put into operation, the domestic supply increased, the PTA cash flow began to compress significantly, and the price fell all the way. 1.4. The third stage (6-10 months price range shock) In June, the price of PTA was driven by the overall rise of bulk commodities. Both futures and spot prices rose. However, compared with other chemical products, the price increase of PTA is still limited, and some devices have glitch. In the PTA market, the selling pressure was heavier in July, but the support of individual equipment failure parking and the rising atmosphere of the entire commodity market made the PTA price maintain a weak shock. In August, PTA was mainly affected by the rise of crude oil and the reduction of production by polyester enterprises before the G20 summit. The price was first raised and then suppressed. In September, there were more centralized maintenance of the equipment. After the G20, the polyester load increased, which boosted the price. However, due to the restart of some units, the supply increased. During the 11th period, crude oil prices rose, the commodity market was strong, and the rotation of funds made PTA prices follow up, but many factories were interested in selling. 1.5. The fourth stage (11-12 months price center shift) In November, despite the sharp fall in futures prices, PTA prices have steadily increased as a whole in the case of capital speculation and accidental overhaul of some PTA plant installations. In December, the downstream polyester industry has entered the traditional low demand season, but the construction load is still high, the polyester factory inventory has dropped to a historical low, production and sales have maintained good, plus OPEC reached a production reduction agreement at the end of November, and non-OPEC countries are active In response to the reduction in production, oil prices continue to hit new highs, and the upstream and downstream jointly promoted the PTA price to break high. Chapter 2 2016 upstream PX operation 2.1. PX price and spread analysis Figure 2.1.1 shows the trend of PX price in 2016. It can be seen that except for the small fluctuation of PX price in the first quarter, it basically oscillates for a long time between 780-830 USD/ton. At the end of December, due to the agreement between OPEC countries and non-OPEC countries to reduce production, the price of crude oil soared. As a result, PX prices began to rise rapidly, breaking through the high point of the year to reach 852 US dollars / ton. Figure 2.1.1: 2016 PX and Brent crude oil futures price trend (unit: USD/barrel, ton) Source: Wind & South China Research Judging from the spread between PX and naphtha, three spreads in 2016 were compressed to around $350/ton, in January, the end of May and October. The rest of the time spreads well, with an average of around US$400/ton, mainly due to the oversupply in the naphtha market and the continued weakness of the fundamentals. Since the fourth quarter, the price difference between PX and naphtha has remained at around US$361/ton. In December, crude oil rebounded. The prices of naphtha and PX both rose sharply, but the spread has a big trend, mainly due to the benefit. Downstream polyester products have risen and stocks are low. The average spread between PX and naphtha in 2016 is expected to be around US$395/ton. Figure 2.1.2: 2016 PX and Naphtha Price Trends (Unit: USD/ton) Source: Wind & South China Research In addition, we review the monthly average data of PX and naphtha spreads from 2014 to 2016. The spreads in 2014 fluctuated greatly. The highs appeared in July and August, reaching around US$456/ton. The spreads in 2015 and 2016 were relatively small, with the spread in 2016 being better than the previous two years, up by about $50 from 2015, and the spreads in March, July and August reaching $427/ton. . Figure 2.1.3: The average monthly price difference between PX and naphtha in 2014-2016 Source: Wind & South China Research 2.2. PX global capacity distribution By the end of 2016, PX's global production capacity has exceeded 50 million tons, most of which is concentrated in Asia, and Asia's PX capacity accounts for around 83% of the world. In Asia's capacity distribution, China's top position is 27%, followed by South Korea and Japan, and China's share of PX capacity in Asia is nearly 34%. Figure 2.2.1: Global PX capacity distribution Source: Wind & South China Research Due to the rapid expansion of PTA capacity in China in recent years, the demand for PX has increased greatly. From 2011 to 2013, China's PX import growth rate to other parts of Asia has reached more than 40%, which effectively promoted PX in other parts of Asia. Capacity development. By 2016, PX's capacity growth rate has slowed down. So far, only a set of 2.3 million tons/year PX unit is expected to be put into production. The actual supply is in 2017. The additional PX capacity increase is that the PX unit of Singapore's Jurong aromatics 800,000 tons/year was restarted in August this year. Table 2.2.1: Possible PX production plan for 2017 (unit: 10,000 tons) Source: Hiroshi Research & Nanhua Research Due to the relatively complicated approval of PX projects in China, most of the PX production capacity is postponed, and China is also a big PX demand country. Therefore, the import dependence on PX is still very high at around 55%. The high import dependence makes China's PX users lose their pricing power for PX. From the source of imports, South Korea is still the largest country to import PX into China in 2016, accounting for 47%, followed by Japan and Taiwan, accounting for about 70% of total imports. From the overall perspective of 2016, the Asian PX market is more profitable. Although the spread in the fourth quarter has been compressed, the overall profitability is still good. For 2017, China is still the largest importer of PX. Although two sets of equipment are planned to be put into operation in the second half of the year, it is still uncertain. The probability of resumption of production of Tenglong aromatics is also small in the short term, so the domestic PX supply is basically There is no growth. If the newly added equipment from India, Saudi Arabia and Vietnam will be put into production as scheduled, there will be a slight surplus corresponding to the new production of China's PTA. However, if the Far East and Xianglu are able to resume production, the domestic demand for PX will increase, Asia. The PX supply and demand pattern will maintain a high probability. Chapter 3 2016 PTA Market Operation Analysis 3.1. Distribution of PTA capacity at home and abroad At present, the world's major PTA production capacity is distributed in Asia, while Asia's PTA capacity is mainly concentrated in China. By the end of 2016, China's PTA capacity accounted for about half of the global PTA's total capacity, accounting for about 60% of Asia's total PTA capacity. According to China Chemical Fiber Information Network, since June 2016, the actual domestic production capacity of PTA has reached 46.13 million tons, the capacity of South Korea has been 5.77 million tons, and the capacity of Taiwan in China has reached 3.25 million tons, occupying the top three in the world. Figure 3.1.1: Global PTA capacity distribution Source: Wind & South China Research In terms of new capacity, most of the new PTA's new production capacity in recent years is concentrated in Asia, with China's new capacity accounting for more than half, so China is the most important PTA production and consumption country. Judging from the distribution of domestic PTA capacity, the capacity distribution of PTA has been concentrated so far, mainly concentrated in coastal provinces and cities, and mainly mainly private enterprises. According to the region, the total production capacity of China's PTA is currently 46.13 million tons, mainly concentrated in Zhejiang, Jiangsu, Liaoning and Fujian. Among them, the PTA plant of Xianglu Petrochemical in Fujian is expected to be postponed in 2017, and Jialong may be postponed. The petrochemical PTA plant is also unstable, and it is reported that parking may begin in January next year. Figure 3.1.2: Distribution of China's PTA capacity Source: Wind & South China Research 3.2. Domestic production capacity and maintenance At the beginning of 2016, China's PTA effective capacity was 43.93 million tons. This year's domestic PTA's new capacity is only 2.2 million tons of Hanbang Petrochemical Phase II. The current operating load is about 90%, and the original planned to be put into production in 2016. The 1 million tons/year PTA plant was not opened as scheduled. As of the end of 2016, the domestic PTA capacity was 46.13 million tons, and the production capacity showed a negative growth with a growth rate of -1.7%. Figure 3.2.1: Distribution of China's PTA capacity (unit: 10,000 tons) Source: Wind & South China Research In recent years, there have been PTA installations for reasons such as cost problems and accidents. In 2015 alone, there were 3.2 million tons in the Far East, 4.5 million tons in Xianglu, 600,000 tons in Jialong and a total of 8.3 million tons in PTA capacity. The closure of the PTA has led to a decline in the actual production capacity of the PTA, which has also alleviated the problem of oversupply of PTA at that time. Table 3.2.1: PTA long-term parking devices in mainland China Source: China Chemical Fiber Information Network & South China Research In July, due to Zhuhai BP's 1.25 million tons of equipment parking, and Hengli's 6.6 million tons of short-term parking, the load plummeted to around 60%. In addition, due to the G20's demand for the reduction of production of polyester enterprises, some PTA companies intensive maintenance in September and October caused a significant drop in load, but overall this year's load is higher than last year. Statistics So far, the average starting load of China's PTA industry in 2016 is around 70%, which is nearly 5% higher than last year. Figure 3.2.2: Domestic PTA start-up load (unit: %) Source: Wind & South China Research In 2017, there are not many new domestic production capacity, mainly due to the delay of Sichuan Yuda and Jiaxing Petrochemical Phase II, which will be postponed until next year. The actual start-up time of Sichuan Yuda may continue to be postponed, and the fastest progress of Jiaxing Petrochemical will be next year. The bottom-up production will not be postponed until 2018, so the impact on the market next year will be relatively limited from the perspective of new capacity. What may have a greater impact on PTA supply next year is the restart of several units of pre-parking, including Far Eastern Petrochemical, Xianglu Petrochemical and Pengwei Petrochemical. After the acquisition of Far Eastern Petrochemical, it is rumored that it will restart the 1.4 million tons/year of the equipment. If the restart is successful, it will have a certain impact on the market supply. Xianglu Petrochemical also reported that it will restart next year, but it is reported that the restart plan will be postponed and the uncertainty will increase. Table 3.2.2: Increase and decrease of domestic PTA capacity in 2017 Source: China Chemical Fiber Information Network & South China Research 3.3. Analysis of supply and demand pattern of PTA industry The domestic PTA production in January-November 2016 was about 29.8 million tons, an increase of 1.4 million tons from the same period in 2015, a year-on-year growth rate of about 5%. At the same time, the average starting load of domestic PTA in January-November was 70.4%, which was higher than that in 2015. On the other hand, from the perspective of the import volume of PTA, due to the overcapacity of domestic PTA in recent years, the supply side pressure appears, the PTA import volume gradually declines, and the PTA import volume in 2016 continues to decline. According to statistics, the PTA imports from January to October 2016 The volume was 389,000 tons, down 172,000 tons from 2015. Figure 3.3.1: Domestic PTA monthly production and operating rate in 2016 (unit: 10,000 tons) Source: Wind & South China Research In terms of social inventory, thanks to the high starting load of polyester, the demand for PTA is better. This year, the domestic PTA industry is in the process of continuous destocking. Although the destocking rate is less than last year, the inventory accumulation at the end of the year is also less than last year. . Figure 3.3.2: Domestic PTA supply and demand pattern in 2015-2016 (unit: 10,000 tons) Source: China Chemical Fiber Information Network & South China Research On the demand side, the year-on-year growth of polyester production in January-October 2016 was 2.2%. The demand for PTA was better than last year, but the production of PTA also increased compared with last year. In addition, the growth of PTA's exports this year is also limited, so the overall view is seen. At the end of 2016, the social inventory of PTA increased slightly. Figure 3.3.3: Changes in domestic PTA supply and demand in 2008-2016 (unit: 10,000 tons) Source: Wind & South China Research As can be seen from Figure 3.3.3, China's PTA capacity has experienced explosive growth in 2012, and the capacity growth rate has reached about 65%. After 2014, the capacity growth rate slowed down, and even in 2016, there was even negative growth. Along with the increase in production capacity, the import volume has decreased year by year and the import dependence has decreased. The import volume of PTA has also increased slightly in recent years. The total supply of PTA in January-October 2016 was 27.26 million tons, and the actual domestic demand for PTA was 27.19 million tons, which basically achieved a balance between supply and demand, and social stocks were lower than last year. Figure 3.3.4: Changes in PTA warehouse receipts in 2015-2016 (unit: Zhang) Source: Wind & South China Research This year's PTA warehouse receipts have gradually increased since March, and reached 750,000 tons in July and August, setting a record high, significantly higher than the same period last year. At the same time, after the delivery of the main contract in September, the number of warehouse receipts rose rapidly. Figure 3.3.5: Changes in domestic PTA inventory in 2014-2016 (unit: day) Source: Wind & South China Research In terms of inventory, PTA factory inventory has decreased significantly compared with the previous two years, and has remained at a low level for a long time, while the inventory of polyester plants has increased from the low level at the beginning of the year to May, mainly for the G20 to catch up and prepare for the goods in advance. In the fourth quarter, factory inventory began to decline, which also indicates that downstream demand has been maintained well this year, and inventory pressure is not large. Table 3.3.1: China's PTA supply and demand balance sheet for 2014-2017 Source: China Chemical Fiber Information Network & South China Research Remarks: 1.2017 data is preliminary estimate 2. Capacity is the end of the year capacity Table 3.3.1 is the balance of supply and demand of China's PTA industry from 2014 to 2017. The 2017 data is forecast data. In 2017, PTA capacity and production are expected to increase slightly. Import volume remains low and the export volume is increased due to capacity in India. The growth rate is expected to decline, the consumption growth rate is estimated to be 4.2%, and the import dependence continues to decline. 3.4. Spread structure In terms of current price difference, futures continued to rise, and spot prices continued to fall below futures prices, reflecting the continued pressure on PTA supply. In terms of inter-period spreads, during the 2016 period, the structure of the distant moon was basically presented. It can also be seen that the market expects the future relatively well. Figure 3.4.1: 2016 PTA current price difference trend Source: Wind & South China Research Figure 3.4.2: 2016 PTA Intertemporal Spreads Source: Wind & South China Research Chapter 4 Operation of the downstream polyester industry 4.1. Capacity production of polyester In 2016, China's polyester market rebounded after it stabilized. The total demand of the industry maintained steady growth at a low speed. Some long-term loss-making devices on the supply side have gradually withdrawn from the market. The overall supply and demand pattern has been moderately improved, and the benefits of polyester products have also improved. Figure 4.1.1: Capacity growth of China's polyester industry in 2011-2016 (unit: 10,000 tons) Source: Wind & South China Research According to China Chemical Fiber Information Network, China's polyester production capacity was 45.15 million tons at the end of 2015. In 2016, the newly added polyester production capacity was 1.73 million tons. Excluding long-term parking equipment, the effective production capacity of polyester in the country at the end of 2016 was 45.85 million tons. , an increase of 1.6% over last year. Table 4.1.1: The situation of China's polyester plants in 2016 Source: China Chemical Fiber Information Network & South China Research The growth rate of polyester production capacity has continued to decline from 15.6% in 2012, and the growth rate in 2016 is only 1.6%. It can be seen that the de-capacity effect of the polyester industry is quite significant, although in recent years there have been many new polyester installations. Both speed and range have been significantly slower than in the previous period, and some long-term loss devices have gradually withdrawn from the market. This year, China's actual production capacity of polyester was put into 7 sets of equipment, totaling 1.73 million tons, mainly supporting polyester filament yarn, polyester bottle sheet and polyester film. The newly added capacity plus long-term parking facilities was 1.18 million tons. By the end of 2016, China's effective polyester production capacity was 45.85 million tons, an increase of 1.55% compared with 2015. From the perspective of the type of equipment placed, it is mainly 1.23 million tons of supporting filaments, accounting for 71% of the total production capacity of polyester; 300,000 tons of equipment for supporting polyester bottles, accounting for 17% of new capacity; The installed capacity is 200,000 tons, accounting for 12% of the new capacity. Figure 4.1.2: Monthly production and load of polyester in China in 2016 (unit: 10,000 tons) Source: Wind & South China Research In 2016, the total output of polyester in China was about 36.4 million tons. This year, it was affected by the G20 summit. Before August, the starting load of polyester was maintained at a high level. Until August and September, the production reduction policy was implemented, and the polyester start load fell to around 75%. . At the end of the G20 summit, the polyester load quickly recovered to more than 80%, and continued until the end of the year, which was mainly affected by better downstream demand for polyester and low inventory levels this year. 4.2. Benefits of various polyester products In 2016, as a whole, the prices of various polyesters in the beginning of March did not fluctuate after a wave of increase. Until the beginning of the fourth quarter, the prices of various polyester products followed the price of raw materials, and the increase was large. The profitability of polyester products improved significantly throughout the second half of the year, especially near the end of the year. The cash flow of individual varieties exceeded 1,000 yuan/ton. Figure 4.2.1: China's polyester product price trend in 2016 (unit: yuan / ton) Source: Wind & South China Research This year, affected by the G20 summit, polyester-related companies have significantly reduced production, and overall supply has decreased. In addition, downstream demand has improved, and the prices of bulk commodities such as crude oil have rebounded. The cost has gradually increased and product benefits have improved significantly. Among them, the most obvious improvement is polyester filament. The average cash flow of POY in the second half of the year is about 200-300 yuan / ton, while the average cash flow of FDY and DTY has reached 400-500 yuan / ton. There is also a level of 200 yuan / ton, bottle and slice performance is relatively poor, but compared to 2015 have improved. Figure 4.2.2: Cash Flow Trend of China's Polyester Products in 2016 (Unit: RMB/ton) Source: Wind & South China Research From the inventory level, since 2016, the inventory of various polyester products has begun to decline, especially near the end of the year, sales continued to be driven by downstream stocking and terminal replenishment, and the inventory of polyester factories dropped sharply. Polyester stocks fell to 1-2 days, and short-fibers even had negative inventory. Overall, it is at a low level in recent years. Figure 4.2.3: Trends in China's polyester product inventory in 2016 (unit: day) Source: Wind & South China Research 4.3. Operation of terminal textile and garment Figure 4.3.1: China's textile and apparel exports in 2014-2016 Source: China Chemical Fiber Information Network & South China Research Figure 4.3.2: China's fabric sales in 2013-2016 Source: China Chemical Fiber Information Network & South China Research Figure 4.3.3: China's textile city transactions in 2014-2016 Source: China Chemical Fiber Information Network & South China Research Figure 4.3.4: Year-on-year increase in apparel retail sales in 2014-2016 Source: China Chemical Fiber Information Network & South China Research According to China Customs statistics, from January to September 2016, China’s total exports of knitwear and apparel were US$67.607 billion, a decrease of 7.16% year-on-year, accounting for 33.17% of the total textile and apparel exports of US$203.833 billion. The total export value was US$120.896 billion, a decrease of 7.45% year-on-year, accounting for 59.31% of the total textile and apparel exports of US$203.833 billion. It can also be seen from Figure 4.3.1 that the export of textiles and clothing has been relatively lower than that of the previous two years. However, the domestic sales of apparel retailing has a clear trend in 2016, and the volume of textile city is in the fourth quarter. There is also a clear growth trend. From the sales situation of the terminal fabrics in Figure 4.3.2, the sales situation before the Spring Festival from the beginning of this year is worse than that of the previous year. The sales of fabrics in the second and third quarters also performed in general, but since the fourth quarter, especially in November, the sales of terminal fabrics It started to move slowly and exceeded the average of previous years. Figure 4.3.5: Changes in the load of Zhejiang loom in China from 2014 to 2016 (unit: %) Source: China Chemical Fiber Information Network & South China Research Similarly, from the start-up load of terminal weaving, the weaving load in the first quarter of this year was lower than that of previous years, but the weaving load has been maintained at a high level of 70% and above in the second quarter, and even reached 80% or more at the highest. Only during the G20 summit, the operating rate dropped slightly. This can also explain why the load of polyester has been high this year and the production and sales are hot, and the inventory is low. The main reason is that the demand of the terminal is better. Chapter 5 2017 PTA Market Outlook In the absence of large fluctuations in crude oil prices, the most important contradiction in the PTA market next year is the increase in production capacity and the return of parking facilities. The capacity of the newly added equipment is expected to be 1 million tons. The possibility of resumption of parking facilities is 1.4 million tons of Far Eastern Petrochemical and 900,000 tons of Pengwei Petrochemical, and Xianglu Petrochemical is reported to have uncertainty next year. Then the total capacity increase is about 2.3 million tons, and the output increase is about 1.6 million tons. The capacity growth of polyester is expected to be 4.3 million tons, the output growth rate is calculated at 5%, and the output at the end of 2016 is 36.4 million tons. Then the consumption of polyester to PTA will increase by about 1.56 million tons next year. Therefore, from the perspective of supply and demand, the increase in supply can basically meet the increase in demand. It is expected that there will be no particularly bad or bullish factors on the supply and demand side of PTA in 2017. Of course, some sudden device failures will not be ruled out. At the end of 2016, the stocks of polyester varieties were relatively low. The new capacity of filaments will not increase much next year, and the benefits will continue to improve. There is a possibility that prices will continue to rise. In terms of slicing and bottle flakes, raw material prices will increase, supply pressure, and exports will face anti-dumping. Impact, profits may be suppressed; staple fiber production will continue to grow next year, domestic sales growth space is not as good as filament, and benefits may be compressed. From the perspective of PX, due to the slowdown in production capacity growth of PTA and polyester in 2017, the growth rate of capacity of Asian PX is expected to exceed the growth rate of polyester demand. PX may not be able to get rid of the weak pattern, but the profit margin at the end of 2016 Will still be maintained. However, as the price of the crude oil end price continues to move upwards, and the probability of a large breakthrough is not large, there will be pressure on the PTA cost end. The rigid demand of the downstream polyester will continue to be maintained in the first quarter of next year, that is, the downstream support is strong. Therefore, PTA prices will continue to be neutral in the next year, and the price center may move upwards. The magnitude will depend on the increase in crude oil prices. The probability of PTA price focus will be slow and upward next year. However, due to the pressure of over-the-counter speculative funds and short-selling sets, PTA prices are difficult to get out of the continuous trend, and the unilateral strategy is more risky. In terms of arbitrage, due to the optimistic expectation of the distant moon, we can consider the reverse arbitrage of the near and far months. South China Futures Optical Metal Frame,Metal Optical Frames,Round Metal Optical Frames,Square Metal Optical Frame Wenzhou 101 optical Co. Ltd , https://www.101optical.com